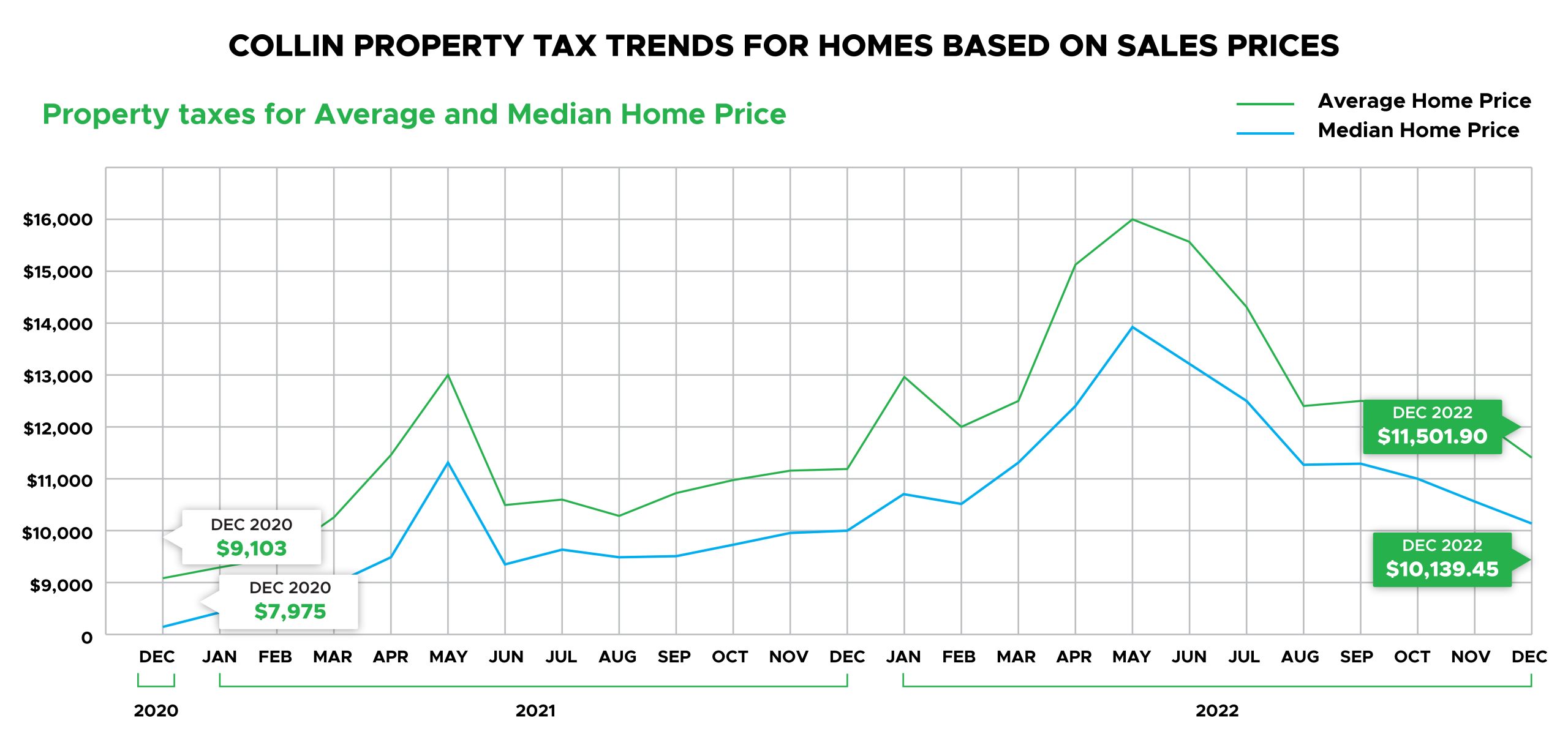

Collin property taxes are based on the market value of property as of January 1 of each year. The above graph documents what annual property taxes would be based on the average / median Collin home price for December 2020 to December 2022.

Collin Property Tax / Home Price Takeaways

- Collin property taxes for average priced home were on a trajectory for huge increases from December 2021 through May 2022.

- The trendline for Collin property taxes peaked in May 2022 and have been on a downtrend since.

- Collin 2023 property taxes for houses are likely to be similar to 2022 tax year based on current trends in Collin home sales.

- The average / median home price estimated for January 2023 will be similar to the price in January 2022.

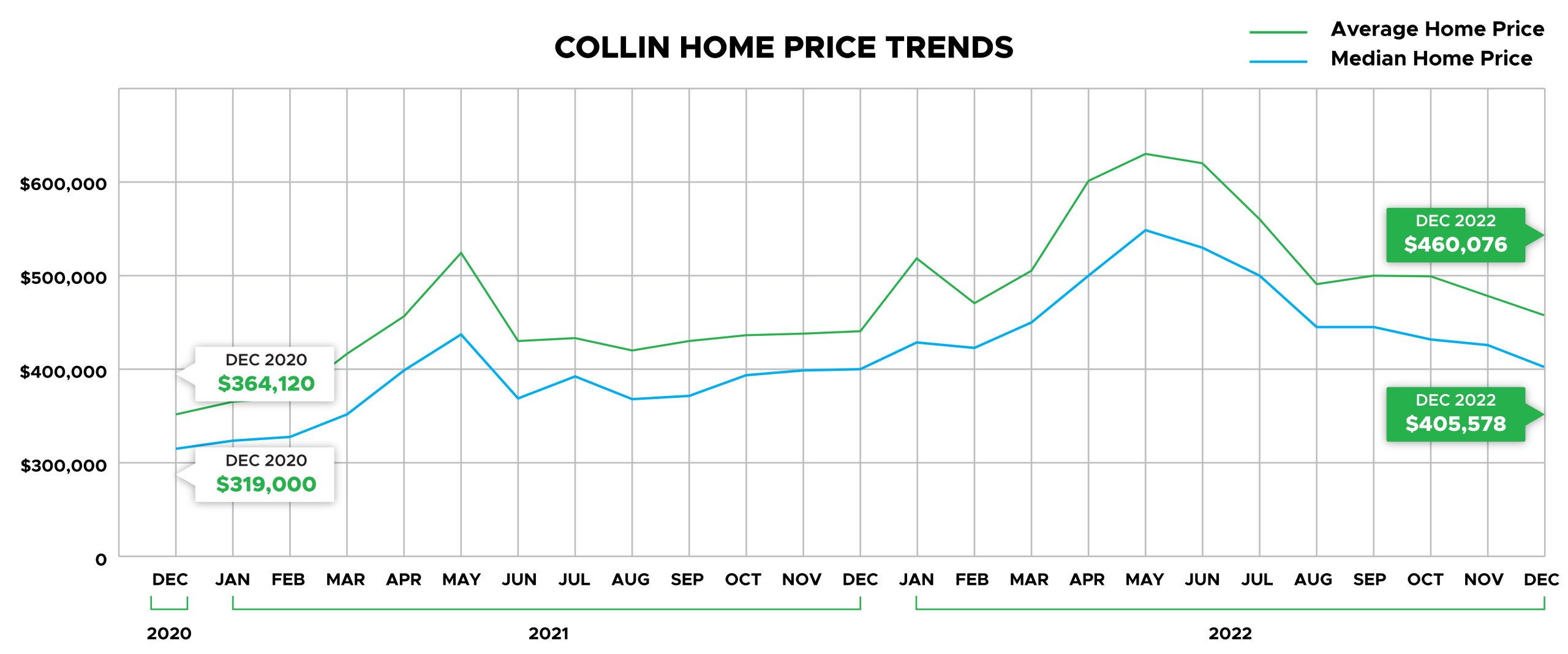

Collin Home Price Takeaways

- Collin home prices were rocketing upward at 8% per month during 2021 and the first 5 months of 2022.

- Collin home prices peaked in May 2022 and have been declining at 3% per month through December.

- Collin home prices are likely to decline further before stabilizing.

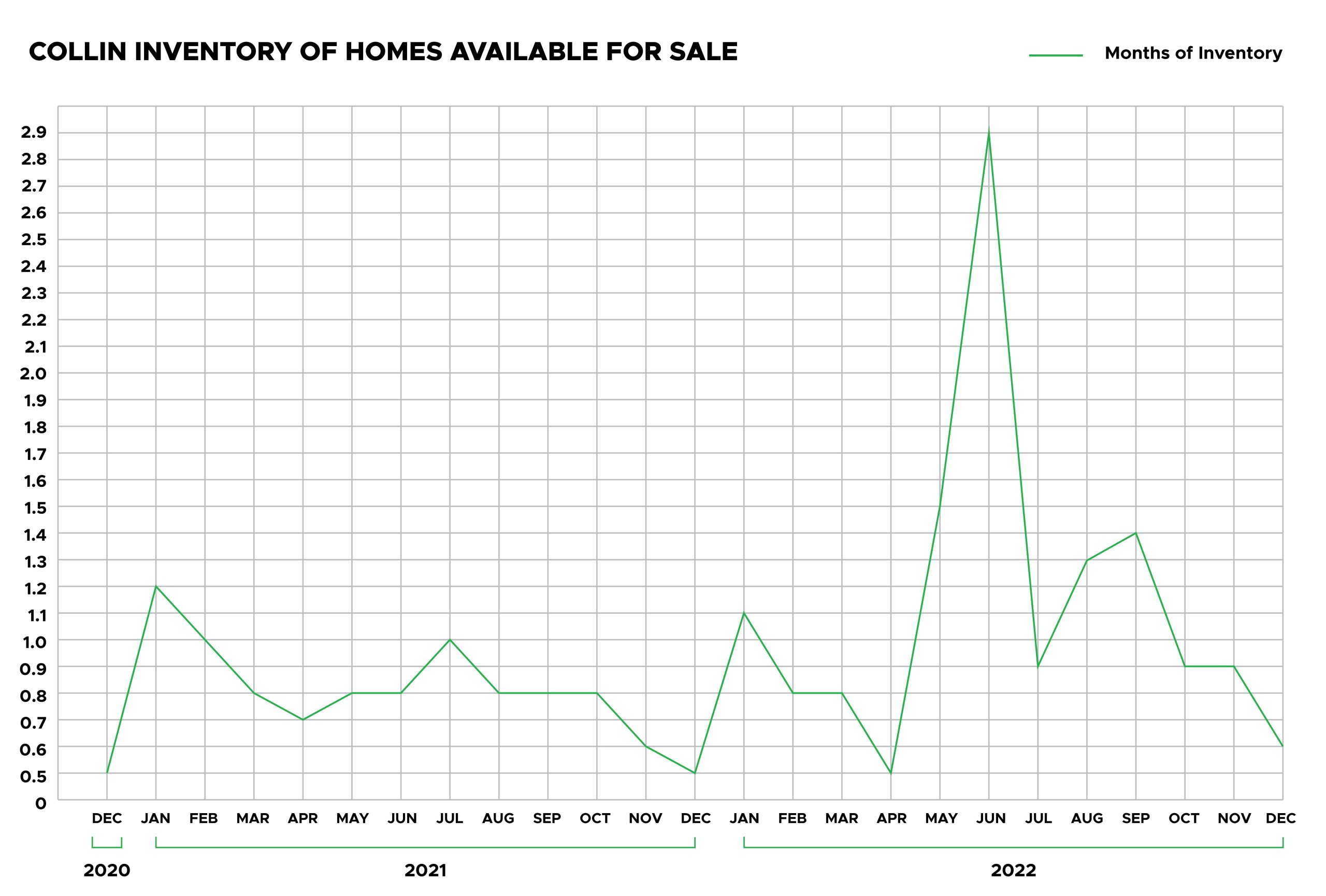

Collin Home Price Inventory for Sale Summary

-

Collin has had one of the tightest home markets with only 0.8 months of inventory for 2021 and 0.9 for the first 5 months of 2022.

-

The inventory of Collin homes for sale has increased to about 2.9 months but is still only one third of the level considered balanced, where neither the buyer nor seller has an advantage.

-

Homeowners are less likely to list homes to sell due to higher mortgage rates than most are paying. Collin homeowners are also trying to process the whipsaw changes in the housing market.

IMPACT OF NATIONAL TRENDS ON COLLIN PROPERTY TAXES AND HOME PRICES

Property Tax Outlook

Property taxes for houses likely peaked in mid-2022. In most major metropolitan areas, year-end 2022 home prices will be similar to home prices at the end of 2021. Since property taxes are based on the January 1 value in most states, property taxes will likely be essentially flat in 2023. It is not clear if appraisal districts will increase values despite the flat trend for home values.

Housing Super-Market Caused by COVID is Over

When COVID hit in March 2020, houses prices plummeted for a month or so and then recovered. The desire to gain physical proximity from neighbors drove many households from huge cities to smaller cities. Mega-markets such as San Francisco, Los Angeles, Chicago, and New York saw a substantial outmigration during the early phase of COVID. Both the level of contagion and morbidity were not well understood for 18 to 24 months. Households fled to small cities. They fled from high density multifamily to single family.

The inventory of homes for sale is measured in months of inventory. Given the pace of home sales, how long would it take to sell all homes. The national trends for inventory of homes for sales have whipsawed from 3.0 in December 2019 to 1.9 in December 2020 and back up to 3.1 in October 2022. A balanced market is considered 6 months of inventory; double the current level.

National home sales in October 2022 are down 28.4% from October 2021. However, let’s be clear. The housing market is still strong. Demand to buy houses is strong but many buyers have been priced out of the market by a combination of high home prices and much higher interest rates.

Higher Interest Rates are Dominating Disruption in Housing Boom

Mortgage rates for owner occupied homes were just under 3% at the beginning of 2022. They are currently in the range of 6.5 to 7%; double the level just 11 months ago. The cost of owning a house is much higher than it was in early 2020 due to: 1) higher home prices, 2) higher interest rates and 3) higher property taxes (driven by higher home values). The median price of a home in the U.S. was about $275,000 in early 2020 versus $379,000 in October 2022 (National Association of Realtors). Home prices are up about 38%; interest rates are up about 100%. The portion of households who can afford a median priced home has fallen by about 40 to 45% since early 2020. Many of these households want to purchase a home. Their income is just not sufficient to buy a home that meets their minimum requirements.

Factors Supporting Prices in Housing Market

While the level of housing affordability has plummeted, the housing market is still tight.-

The inventory of home for sale, at 3.1 months, is only half of what is considered a balance market (6 months).

-

The supply of homes for sale is being artificially limited by homeowners who would like to sell and buy another home. However, with an interest rate of around 3%, they simply could not afford a mortgage for a new home at 6.5 to 7.0%

-

The inventory of new homes for sale is relatively high compared to the pace of purchases. However, home builders are racing to reduce both their inventory and new homes under construction. Some home builders are discounting by 20% for bulk sales to investors.

-

Home purchases by investors are off 30%. Investors are impacted by high interest rates, higher home prices and higher property taxes.

-

There is pent-up demand to buy houses. Assuming interest rates decline over the next 2 to 4 years, many households will enter the market and purchase homes.

-

The labor market has remained strong despite diligent efforts by the Federal Reserve to induce slack into the economy.

Factors Negatively Impacting Home Prices

-

Interest rates are likely to remain high for at least 12 to 24 months, and perhaps much longer. The components of cost for a homeowner are primarily:

- Interest

- Property taxes

- Casualty insurance

- Maintenance

-

The is a possibility of a recession in 2023. Most economics forecasters expect a recession will be necessary to reduce inflation to a level satisfactory to the Federal Reserve.

- If there is a recession, employment will fall.

- The rate of homes put under contract and not closing has risen sharply due to higher interest rates and tightening underwriting.

Is a Housing Crash Imminent?

- No, a housing crash is not at all likely.

- It is likely that housing prices will soften during the period of lower affordability.

- The housing crash in 2008 was largely driven by poorly conceived and fraudulent loan underwriting. Lenders have exercised discipline in underwriting loans during this cycle.

- The inventory of homes for sale would likely have to exceed 6 months for a strong down-draft in housing prices. It is not likely the inventory of homes for sale will fall that much in the short term.

Housing Market Conclusions

The boom in higher home prices is over and will not return soon. Much lower interest rates are needed for robust increases in home prices. The pent-up demand for housing will act as a brake on reductions in home prices. Most reductions in home prices are likely during the next 12 to 24 months while the Federal Reserve battles inflation.