The Texas Temporary Exemption for Disaster Damage serves as an important tool to support property owners affected by natural disasters, helping them recover and rebuild their lives and communities. This applies to both businesses and homeowners who have suffered as a result of the disaster.

Qualified Property Types

- Tangible personal property used for income production

- Improvements to real property (this includes the structure or house)

- Certain manufactured homes

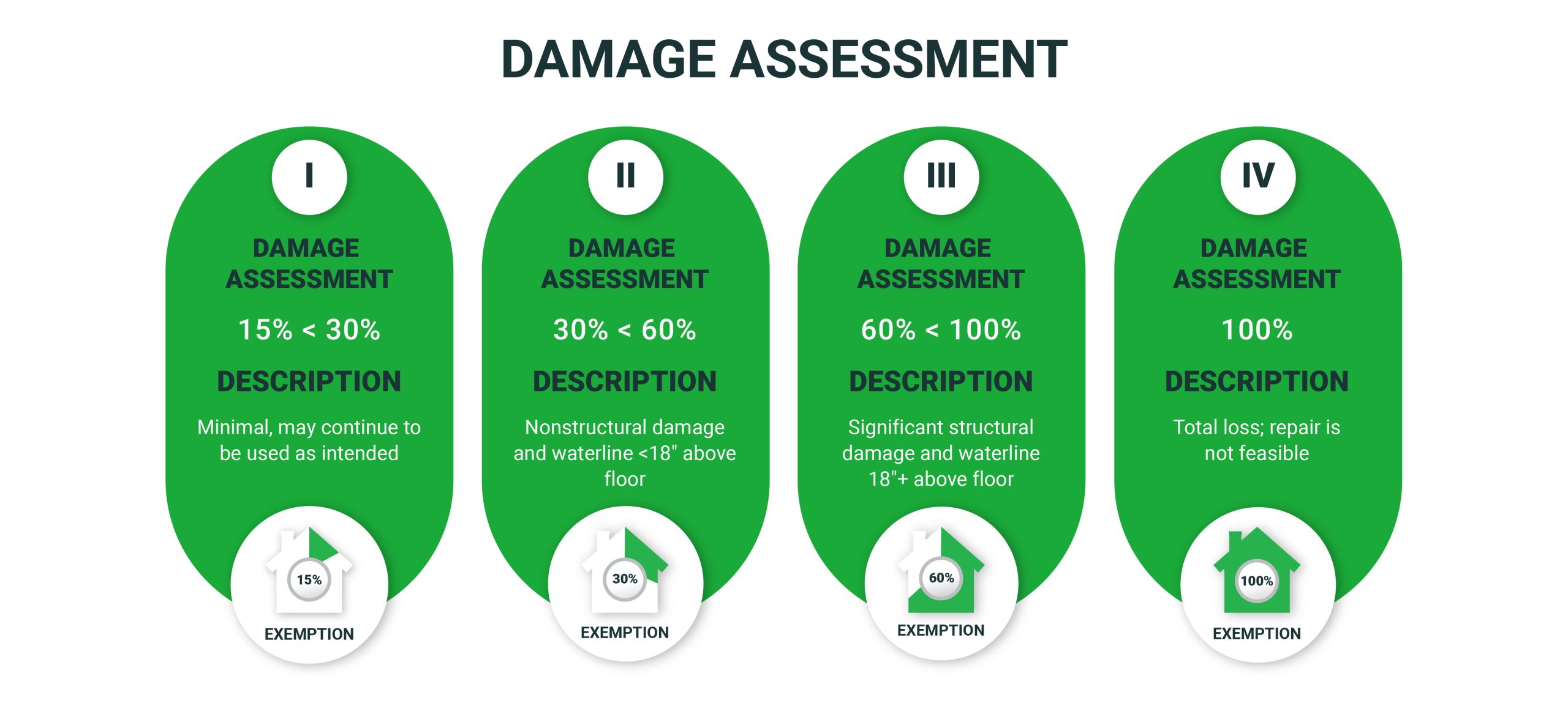

Determining Exemption Percentage

Once a homeowner applies for the exemption, according to Texas Tax Code 11.35, the chief appraiser of the county evaluates the qualification and then assigns a damage assessment of Level I, II, III, or IV, depending on the amount of damage.

Calculating the Exemption Amount

To clarify how this damage assessment will translate into an exemption amount, here is an example calculation:- John Smith is a hypothetical resident of Montgomery County, where Governor Greg Abbott issued a declaration of disaster on April 30, 2024.

- The improvement value of John Smith’s home is $300,000.

- Following the recent flooding event, John learned that the cost to repair his home is $65,000.

- $65,000 Damage/$300,000 improvement value = 21.7%

- John’s 21.7% damage assessment qualifies his damage as Level I, making him eligible for a 15% exemption.

- Because the disaster declaration was issued on April 30, this gives a proration amount of 0.61 to account for the portion of the year where the value of John’s home was diminished. The proration amount is arrived at by taking the number of days remaining in the year after the disaster is declared, 223, and dividing by 366 (2024 is a leap year).

- Take the improvement value x exemption percentage x proration to determine the temporary disaster exemption amount for John’s house.

- In John’s case, it looks like this: $300,000 x 0.15 x 0.61 = $30,150.

- This means that $30,150 is exempted from property taxes for the year 2024.